Singapore T-bills Guide : How to invest using Cash /SRS/CPF

.png)

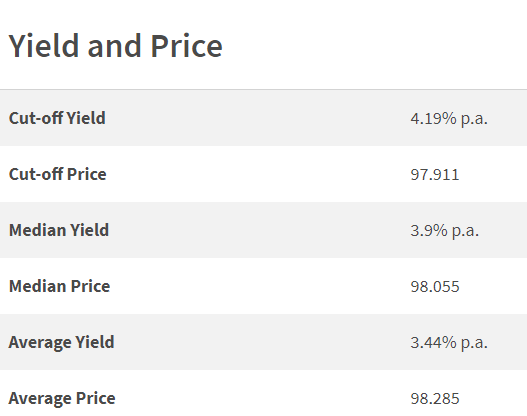

4.19% pa for 6 months!

You are probably reading this because you must have heard that the latest Singapore T-bills for Nov 2022 will give you a return of a whopping 4.19%.

To put things into perspective, a 6-month T-bills issued in May 2022 was only a paltry 1.56%. In just a short 6 months, it has leapt to 4.19%, a rate many would not be expecting. The good thing is that T-bills can be invested using Cash, SRS or CPF. With CPF interest maintaining at 2.5%, the headline rate would not doubt perk the interest of many.

|

| Nov 1 2022 T Bill |

However, those new to T-bills might get lost in financial jargon such as competitive/non-competitive bidding , cut off yield and CDP account. Let us simplify it in this post.

CONTENT

- What are T Bills?

- When and What can I Invest?

- How Big is the Issue Size?

- Any Investment Limit?

- How to use Cash/SRS/CPF to invest?

- Competitive vs Non -Competitive Rates

- HOW TO PREDICT INTEREST RATES

- How to Calculate Returns?

- Would I get Full Allocation?

- HOW TO CHECK ALLOCATIONS

- What Happens upon Maturity?

- HOW to Sell before Maturity?

- Any Risk for T-Bills?

- What are the Charges?

- Should I Invest in T-BillS?

What are T-bills?

Let's start from the basics.

- T-bills are financial instruments ( similar to Fix Deposit) issued by the Government of Singapore.

- It is rated AAA (meaning it is super safe, some say risk-free or Gold Standard!)

- Tenure of 6 months to 1 year.

- Instead of Interest or coupons, the T bills are discounted. Upon maturity, investors will get the face value. What

In layman's terms, it means leading money to Singapore Government and getting extra money back.

Example

.png)

When AND WHAT Can I invest?

T bills for retail investors are available in tranches of 6 months or 1 year. At the time of writing, 6-month T-bills are issued fortnightly, while the 1-year T-bills are issued quarterly.

For 6 months of T-bills, the 2022 schedule is as follows.

For the 1 year T-bills, there are no more allocations for 2022.

You can refer to the full schedule here.

How big is the issue size?

Issue size varies from different tranches. It ranges from $3+ Billion for 1 year T bills and $4+ Billion for 6 months T bills. The size is significantly higher than the popular Singapore Savings Bonds ($900million for the last tranche).

ANY Investment Limit?

The minimum investment is $$1,000. The subsequent investment will be in multiples of $1000

There is no maximum amount an individual can hold, but there are limits for each auction. Also, you can submit up to $1 million in non-competitive bids at each Auction.

HOW tO USE CASH/SRS/CPF TO INVEST?

.png)

Cash, SRS or CPF (Ordinary or Special Account) can use for investment.

How to invest using Cash?

- Bank account with one of the three local banks ( DBS/POSB, OCBC and UOB)

- Individual CDP account with Direct Crediting Services Activate. This allows coupon and principal payments to be credited directly into a bank account. You can open a CDP account here.

- Apply through DBS/POSB, OCBC, and UOB ATMs or Internet Banking Portal

Things to Note

- You cannot buy T bills with a joint CDP account. However, you can edit from a joint account.

- Applications via banks may close 1-2 business days before the auction. Check with the individual banks for the exact cut-off time for the different application channels.

- The full face value will be deducted upon application day. The difference in the final discount price will be refunded on the day of the auction. The balance will be retained for the T-bills. This means you would have lost a few days of interest as the issue date is usually T- 3 Days. Likewise, crediting of funds upon maturity is at T+3 for auction.

How to invest using SRS?

- You will need an SRS account with one of the three SRS operators (DBS/POSB, OCBC and UOB)

- Apply via the bank's internet banking portal.

How to invest using CPF?

CPFIS-OA Application

- You need a CPF Investment Account with one of the three CPFIS agent banks (DBS/POSB, OCBC and UOB)

- The application would be made in person at any branch of the CPFIS-OA agent bank.

CPFIS-SA

- No need to open CPF Investment Account if you wish to invest CPFIS-SA funds

Things to Note

- For first-time applicants to CPFIS-OA, you must be age 18 and above and complete a Self-Awareness questionnaire. Due to current overwhelming requests, it may take weeks or months for CPF-OA to be active.

- You cannot fully use the OA and SA savings. For OA, you can invest after setting aside $20,000 in your OA. For SA, you would need to set aside $40,000

- For CPF funds, unlike Cash investments, only the amount AFTER the discount is deducted from CPF. The deduction is usually T-2 days. The crediting is at T+3 days.

- For the month where CPF is deducted, there will be no interest for that month from CPF regardless of when it is deducted. Depending on the debit and credit dates, you may lose one or two months of interest.

Based on a 2 months lag, a

6-month T-bills would need to be at least 3.33% to break even.

1-year T bills will need 2.92% to break even. This

is for CPF OA.

CPF SA would

require a much higher BE.

- You need to manually credit the funds back to CPF via the CPFIS bank Internet Portal, else the funds will remain in the bank's account. This may further impact the loss of interest from CPF

Competitive Bids vs Non-Competitive Bids

.png)

You can opt for competitive or non-competitive rates during the application process.

|

|

Non-Competitive |

Competitive |

|

Overview |

You specify the amount you want to invest, not the yield |

You specify the amount and the yield you want to invest |

|

Allotment |

Non-competitive bids will be allotted first, up to 40% of the total

issuance amount. |

Note that you may not get the full amount you applied for. It depends

on how your bid compared to the cut-off yield |

|

Reason to Select |

Choose this if you want to invest in the bond regardless of returns or

are unsure how to bid. |

Submit a competitive bid if you only invest in the bond if the

yield is above a certain level. |

Here are the advantages and disadvantages of Non-Competitive vs Competitive bids

|

|

Non- Competitive |

Competitive |

|

Adv |

Do not need to worry about what bid to input. Based on the last few tranches, it most likely will get a full allocation. However, there is a cap of 40% allocated to non-competitive bids. If the amount applied exceeds 40%, the investment may be pro-rated or not allocated. |

Able to determine the minimum yield. This is important for those using

CPF funds, who may have negative returns.

You would still be given the same interest rates as non-competitive

even if you bid lower. This is because T-bills are based on Uniform

Price Action.

|

|

Dis-adv |

No Protection against Black Swan Event. If the rates crash, you will have to accept the rates provided.

May not get full allocation if oversubscribed.

|

You will not get an allotment if your bid is higher than the cut-off yield. |

How to predict the interest rates?

|

Date |

12 Wks MAS Bills |

6 Months T Bills |

|

23 Sep |

3.32% |

|

|

29 Sep |

|

3.32% |

|

11 Oct |

3.8% |

|

|

13 Oct |

|

3.77% |

|

26 Oct |

4.35% |

|

|

27 Oct |

|

4.19% |

While we do not have a crystal ball, we think the 12 weeks MAS bills ( only available to institutions) would be the closest gauge. Do note that interest rates will only be determined on auction day.

You can check the MAS bills rates here

To check the potential of future rates, look at the US Interest rates. Singapore tends to follow a similar path, so if US looks set to increase rates, Singapore will do so as well.

How to calculate returns?

Use this formula to calculate returns.

(100 - Discounted Price) x 365 / No of days held = Interest rates.

Round it down to the last 2 decimal points.

Would I get the full allocation?

It would depend on a few factors. Are you bidding on non-competitive or competitive terms (see above). Additionally, for non-competitive, it would be dependent if the allocated % of the tranch has been oversubscribed.

If oversubscribed, your allocation for non-competitive bids will be prorated as per MAS guideline.

If your bid is below the cut-off yield, you will get your allocation for competitive bids. If your bid is the same as the cut-off yield, you may or may not be allocated depending on the demand and the cut-off point.

How to check for allocation?

- For cash applications, some banks will send SMS. Others will credit your bank account with a discounted refund. You can also check the CDP statement after the issue date.

- You can check the SRS operator's statements for the SRS application.

- For the CPFIS-OA application, you can check the CPFIS statement sent by agent banks or online. You can also check your CPF account for the deduction.

- For CPFIS-SA, you can check your CPF statement after the issue date.

What happens upon maturity?

Cash and SRS will be credited back to the respective bank's account. For CPFIS-OA, it will be credited back to CPF-IS OA account with the bank. You would need to request to transfer back to CPF manually.

How to sell before maturity?

There is no early redemption for t-bills, but you can opt to sell on the secondary market at DBS, OCBC or UOB main branches. It is best to hold them to maturity as prices may fall before maturity, and with low trading volume for T-bills, they are rather illiquid.

Any Risk for T bills?

As with any financial instruments, T- bills come with risk. One of them would be early redemption. Another will be re-investment risks, given its relative short-term and interest rate volatility.

Nonetheless, T-bills are considered low risk is given that it is backed by Singapore Government, a AAA credit-rating country.

What are the charges?

Some banks would charge a fee for each application request. Do check with respective banks on the charges.

Should I invest in T bills?

.png)

T-bills will be one of the best options if you want a short-term, low-risk financial product to park your funds. In some circumstances, the returns could be higher than fixed deposits. With rising inflation, T-bills provide a possible hedge.

Nonetheless, consider alternatives like Fix Deposit, Singapore Savings Bonds or longer-dated SGS Bonds. All these instruments differ in tenure, redemption and opportunity costs. Choose one that best fits your needs.

TWD is a self-funded website.If you like our work, you can buy us a coffee.

Your support will help keep us going!

Disclaimer

The information provided by TWD serves is for educational purposes. It is

not meant to be personalised investment advice. Readers must do their due

diligence and refer to financial advisors for their investment needs. The

information is correct as of 28 Oct.

No comments