Singapore Savings Bonds Jan 2023 - 2.97%: Worth investing?

.png)

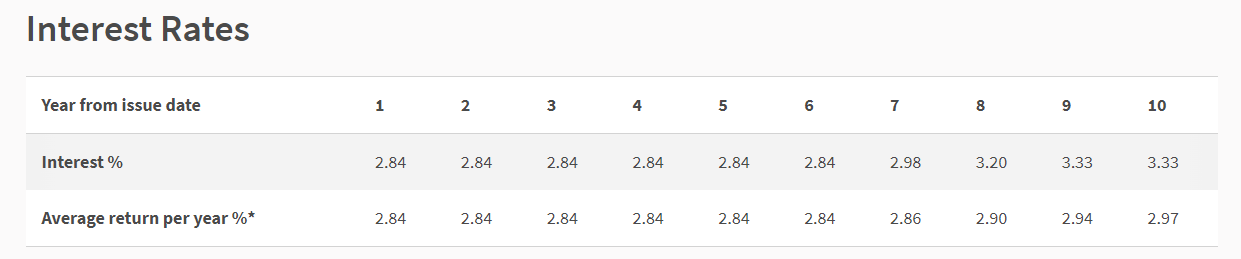

Singapore Savings Bonds slide below 3% for the new year.

At 2.97%, it is lesser than Dec 2022 SSB rate of 3.26%.

For every 100,000 invested, this would mean a difference of $2900 over 10 years.

The rates are as follows.

|

| Source: MAS |

At this rate, one can consider other short-term and long-term options.

SGD Fixed Deposit

Banks are offering more than 4% for a yearly deposit. For example, RHB is offering 4.1% for a 2-year FD.

|

Financial Instrument |

Returns |

Net Returns |

|

SSD (2 Years) |

5.68% |

$5,680 |

|

RHB FD (2 Years) |

8.1% |

$8,100 |

In comparison with SSD, RHB FD offers an additional $2,420 return

Singapore 6 Months T bills

The last 6 months' T bills offer 4.28% for the last auction.

|

Financial Instrument |

Returns |

Net Returns |

|

SSB (6ms) |

2.84% |

$1,420 |

|

6 Mths T Bills |

4.28% |

$2,140 |

At this rate, over a 6 months period, you will gain $720. Over 1 year, if the t bill rates hold, the extra you will earn from 6 months of T bills will be $1,440.

SSB vs FD vs T Bills

.png)

The difference between the financial instruments lies in their liquidity and what would happen if you redeem it early.

Singapore Savings Bonds (SSB)

You are allowed to redeem at any time. The Principal and the interest accrued will be paid after the redemption period. Redemption is allowed every month.

Fixed Deposit (FD)

Fixed Deposits can be redeemed anytime. Unlike SSB, you usually would not get accrued interest based on your FD's original interest rates. You may receive the accrued interest based on board rates or NO interest, depending on how long you have placed the FD. Additionally, you may be charged a penalty for early withdrawal.

T Bills

T bills can be redeemed anytime. However, unlike SSB and FD, you must visit the bank for redemption. Redemption is done in the open market. Thus, there will not be a transparent price for it. You may LOSE part of your principal if the open market price falls below your initial price.

Other than higher interest, you would have to assess if you need the funds at any point during the investment. If you need cash anytime, Singapore Savings Bonds will provide good value as it has the most flexibility for early withdrawal. What to invest in would very much be dependent on what is your intentions for your funds.

Disclaimer

The information provided by TWD serves is for educational purposes. It is

not meant to be personalised investment advice. Readers must do their due

diligence and refer to financial advisors for their investment needs. The

information is correct as of 4 Jan 2023.

No comments