What happens to your CPF at 55?

Turning 55 is a big thing in Singapore.

At that age, one significant financial milestone is the ability to withdraw cash from CPF. After working for a better part of one's lifespan, many look forward to the extra 'cash in hand'.

This is a list of what you can expect for your CPF from 55.

1 Retirement Account (RA)

A Retirement Account will be set up when you turn 55. Funds will first be transferred from Special Account (SA), followed by Ordinary Account (OA) savings.

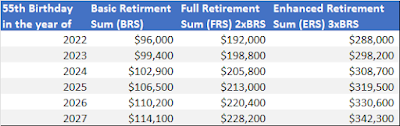

The amount transferred will be up to Full Retirement Sum (FRS). If there is insufficient RA to make up FRS and you have used CPF savings for the property, the amount withdrawn from the property (including accrued interest) will be used to meet FRS (Property Pledge)

It is not mandatory to top up RA if you cannot set aside your FRS. You will receive monthly payout from RA from retirement age. You HAVE to apply to start receiving monthly payouts at any time after 65. Esle payouts will only start automatically at 70.

2 Cash Withdrawal after 55

Regardless of how much you have in CPF, you can withdraw at least $5000 or any amount in excess after setting aside from FRS from 55. The CPF money can be withdrawn at any time in full or partially and as frequently as possible.

If you have sufficient property pledge to cover the Full Retirement Sum, you can withdraw the balances in the CPF SA, OA and any RA savings above the Basic Retirement Sum. The rational for this is that property owners do not have to worry about rent, hence CPF allows withdrawal.

If you are born in 1958 ot later, you can withdraw 20% of your CPF RA savings at age 65 on top of monthly payouts ( This will include the initial $5000 withdrawal at age 55.

Any balance in CPF continues to earn interest rates as follows

- OA: 2.5%

- SA : 4%

- RA: 4% *

CPF monies in RA can earn up to 6%

- First $30,000- 6%

- Next $30,000 - 5%

- Remaining -4%

3 Topping up of RA to full retirement when selling your property

If the CPF used for property has been pledged for RA,the amount will be earmarked for RA and CANNOT be taken out as cash. These will be deducted from your proceeds to Top up RA.

4 CPF Ordinary Account can still be used for Property Loan

If there is any balance in OA, it can still be used for housing loan repayments.

There is a limit to what you can use for a housing loan from OA. Refer to CPF to check on the limits. The limit safeguards against overspending on housing loan repayments at the expense of retirement savings.

5 CPF Ordinary Account and Special Account remain open

As usual, the OA and SA account remains open and will receive employer and employee contributions. The % of the contribution will be reduced from age 55.

6 You can withdraw Retirement Savings if you have other sources of lifelong income

Do you know that you can withdraw all your retirement savings at 55?

You are eligible if you meet the following conditions.

- 55 and above

- Receiving guaranteed monthly payouts from the private annuity (bought with cash or under the CPF Investment Scheme) or pension.

- Both the policyholder and sole insured person of the annuity policy. Multiple annuity policies can be used.

- The full withdrawal is possible if the yearly payout from an annuity or pension meets the payout benchmark. The private annuity cannot be used to obtain a loan.

- Conditions on top-ups to RA apply.

Disclaimer

This post is meant for educational purposes and does not constitute

financial advice. The information was updated on 15 Apr 2023. TWD is not

liable for any errors or changes to the CPF policies. For the latest

CPFguide, do refer to CPF.

No comments