Fix Deposit vs Singapore Savings Bonds vs T-Bills : How to earn high interest in Singapore

.png)

Want to earn high interest for your savings

For the past few years, earning high interest in low-risk products has been almost impossible in Singapore. Save for CPF providing 2.5% for Ordinary Accounts and 4% for Special Accounts, putting money in banks for even bonds will yield marginal returns of 1-2%.

With the recent rise in interest rates, one would have more options today to enhance their yields from savings. The 3 products with the least risk in the market today will be Fixed Deposit, Singapore Saving Bonds and T- Bills. If you are curious about which option is the best for you, here is a summary of each product.

Fixed Deposit (FD)

Fixed Deposits are usually placed with banks in Singapore. A sum of money is blocked for a fixed deposit as per determined by the bank. The interest is provided at the start of the fixed deposit. At the end of the period, you would get back the principal and the interest earned from the FD. Interests are tax exempted.

Currently, one of the highest FD rates over 1 year is provided by RHB at 3.4%. You can check the latest FD rates for Singapore banks here.

Min investment: Usually from $5,000, although some banks prefer a higher amount (eg $20,000). It does not need to be in multiples of $1000

Pros

- One of the easiest ways to get high interest.

- The Deposit Insurance Scheme protects up to $75,000 of your total deposit in the bank.

Cons

- If you need funds, you need to break the FD. Some banks may not provide interest if it is not kept within the agreed period.

- Interest may differ from initial placement and is often much lower if you break your FD early.

- Some banks charge penalties for breaking FD

How to apply?

An application can be made at the bank over the counter or online for selected banks.

Cash is to be used to place Fix Deposit. There are no options for CPF funds. SRS funds may place in FD but at a much lower rate.

Fees

No fees for placement

Suitable For

Those who would prefer fuss-free investment.

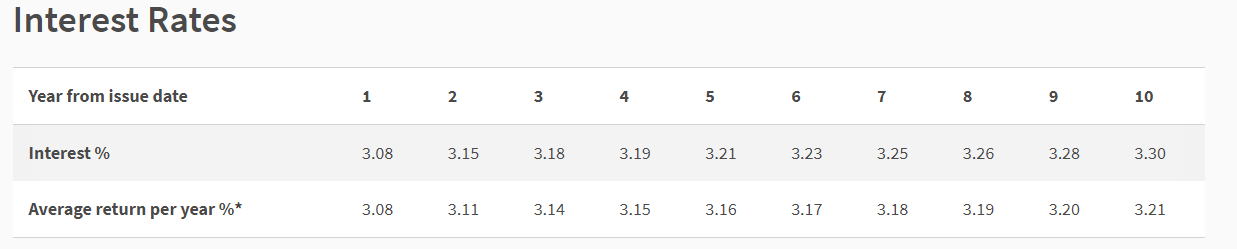

Singapore Savings Bonds (SSB)

.png)

These are issued by Singapore Government with the principal guaranteed by the government. SSB is usually issued for 10 years. Investors will get coupon payments every 6 months, and the coupons tend to increase over time. Returns are tax exempted.

Pros

- Interest will be known throughout the whole 10 years, thus taking out guesswork from investment.

- Investors can withdraw at any given month with no penalty. Accrued interest will be returned today with the principal.

- Investors can choose to reinvest their funds at the new SSB if the cap is not reached.

- Suitable for small amounts.

- SRS funds can be used for investment.

Cons

- Interest rates are locked in, and you may be 'stuck' at a lower rate unless you redeem.

- There is a cap of SGD 200K for the total investment

- 1st-year rate may not be as attractive as FD

- You need an individual CDP account and can only invest with the selected banks (DBS, OCBC, UOB)

- You may not get full allocation if the demand outstrips supply. That would mean some funds will be left idle.

- SRS is open to individuals aged 18 years and above. You need an account with one of the three local banks and an individual CDP account.

- Apply through DBS/POSB, OCBC and UOB ATMs of Internet Banking or OCBC mobile application. SRS investors may apply through their respective SRS Operator's Internet banking

- Redemption can be done in any given month before the bond matures with no penalty. You will be paid principal and accrued interest.

- The application will close on the 4th working day before the end of the month at 9pm.

.png)

Pros

- Short-term investment 6 months or 1 year

- You can opt to choose between competitive or non-competitive bids*

- Small minimum sum

- Can use Cash, SRS and CPF

Cons

- Liquidity risk - You can sell but at market price. The principal is not guaranteed.

- You have to face re-investment risk at a lower rate compared to SRS account.

- May not always get the full amount.

*Competitive vs non-competitive bids

Competitive: You can choose a baseline of what yield you might want to accept. Should the Cut off yield be higher, you will get the T-bill at the cut of yield. In most cases, you should get a full allocation, especially if you place a competitive bid below the stated yield. Do your maths wisely and do not over-commit.

Example

Bid for 3%

Eventual yield: 3.5%

You will get 3.5%

If the eventual yield is less than 3% ( eg 2.95%), you will get nothing.

Non-Competitive: You will accept the cut-off yield from the auction.

How to apply?

You can apply via cash, SRS or CPF.

For cash application

You need a bank account with DBS/POSB, OCBC,

or UOB. You will also need an individual CDP account with Direct Credit

Services activated. Apply via ATM or internet banking.

For SRS application

You will need an SRS account with DBS/POSB, OCBC or UOB. Apply under internet banking portal or the SRS operator

For CPFIS application

For CPFIS-OA, you will need a CPF investment account with one of three CPFIS agent banks ( DBS/POSB, OCBC, UOB). if you are investing using CPFIS-SA funds, there is no need to open any CPD investment account. YOu will need to submit an application in person at any bank of the CPFIS bond dealers.

Fees

$2 per transaction for selected banks. Some banks will also charge for custodian fees on quarterly basis.

Suitable for

Those with a shorter time horizon would like higher rates than FD. This is more suited for well-versed investors due to the requirements.

If you like our work, you can buy us a coffee. Your support will help keep us going!

Disclaimer

This is not intended as investment advice but as information on what is

available.. Each individual has their own risk appetite. For financial

planning, it is best to consult your financial planner for advice.

No comments